Baytex Energy, (NYSE:BTE) made news toward the end of Feb with its announcement of the merger with Ranger Oil Corp (RROC) for about $2.5 bn last week. The market’s initial take wasn’t very favorable as the stock of BTE swooned from its already low level. It has since rebounded, and our hunch is it has farther to run.

This article will analyze the company’s rationale for this deal, which doubles its size in one fell swoop. The market had recently begun forgiving BTE as the news has been digested. An upgrade from TD Cowan didn’t hurt in this regard, but there’s more to it. I think the market will take a fresh look at BTE and boost shares in the coming weeks. It’s happening already as the shares have rebounded from the March 14th low of $3.20 to $3.77 in the premarket today. Notably, they still have further to go to regain their pre-deal level of $4.63. With the crude oil price rebound, this could occur quickly. We think there is an upside beyond that.

Oil inventories are tight globally, and demand is projected to outstrip supply in the second quarter of this year. This isn’t reflected in the NYMEX strip as yet, mostly thanks to U.S. domestic inventories having gained ~60 mm bbls in the last few months. We think current oil prices in the $ 70s will continue higher as the year progresses, consistent with the inventory and supply projections, and create a lift for BTE shares from current levels.

Deal-making in the Eagle Ford

We’ve discussed the M&A frenzy in this play recently in an OilPrice article. In it we documented the big dollars changing hands as acquiring companies look to enhance their portfolios and PE firms cash out. The M&A action over the past year in the Eagle Ford has been just torrid, with nearly $ 3bn in transaction value with just the two companies we mention below.

These companies, Marathon Oil, (NYSE:MRO), and Devon Energy, (NYSE:DVN) have made significant moves in the past half year to enhance their Eagle Ford position with impressive multi-billion dollar acquisitions. Each company has its own rationale, but in general the Eagle Ford has a couple of features that suitors are finding attractive. One is the oil cut. The second is the proximity to the market near Corpus Christie. In that context, the tie-up between Baytex and Ranger makes sense and was probably spurred on by Eagle Ford partner MRO’s recent move in the play (discussed above).

Why is BTE shopping in the Eagle Ford?

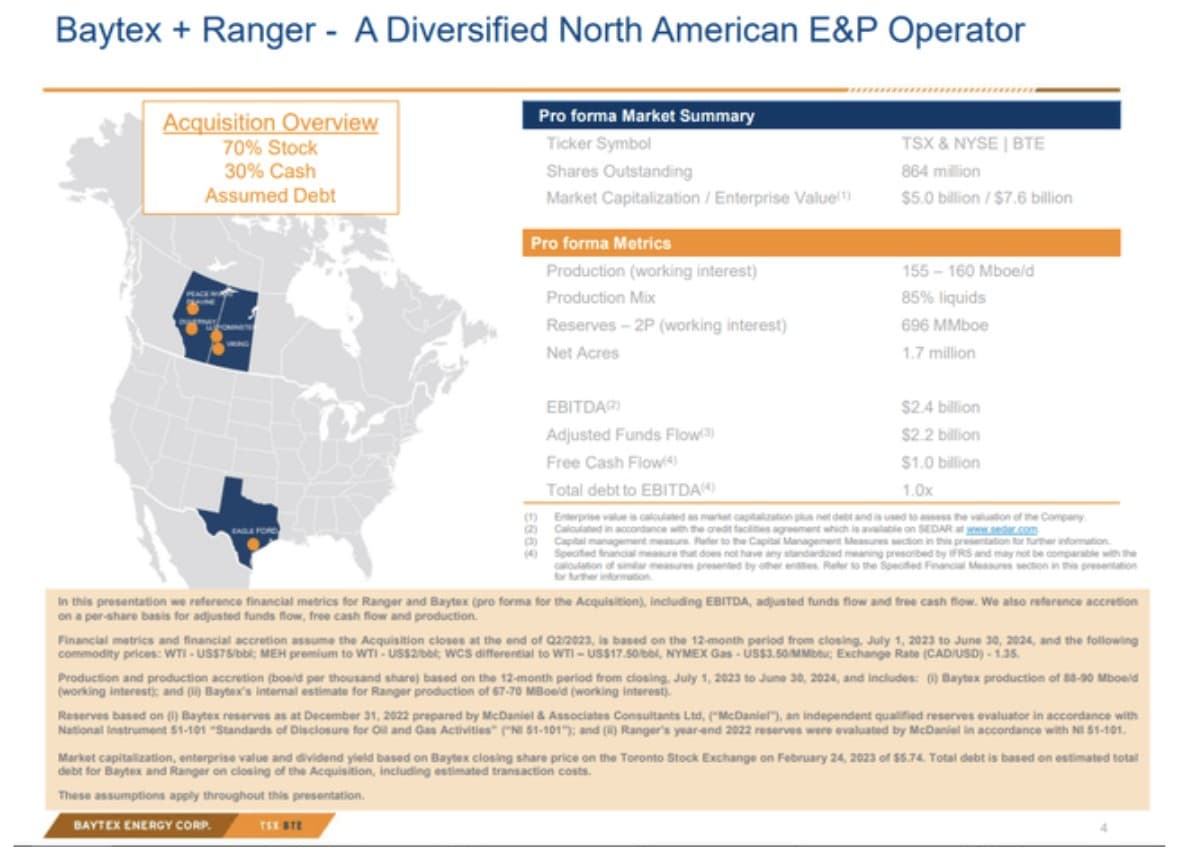

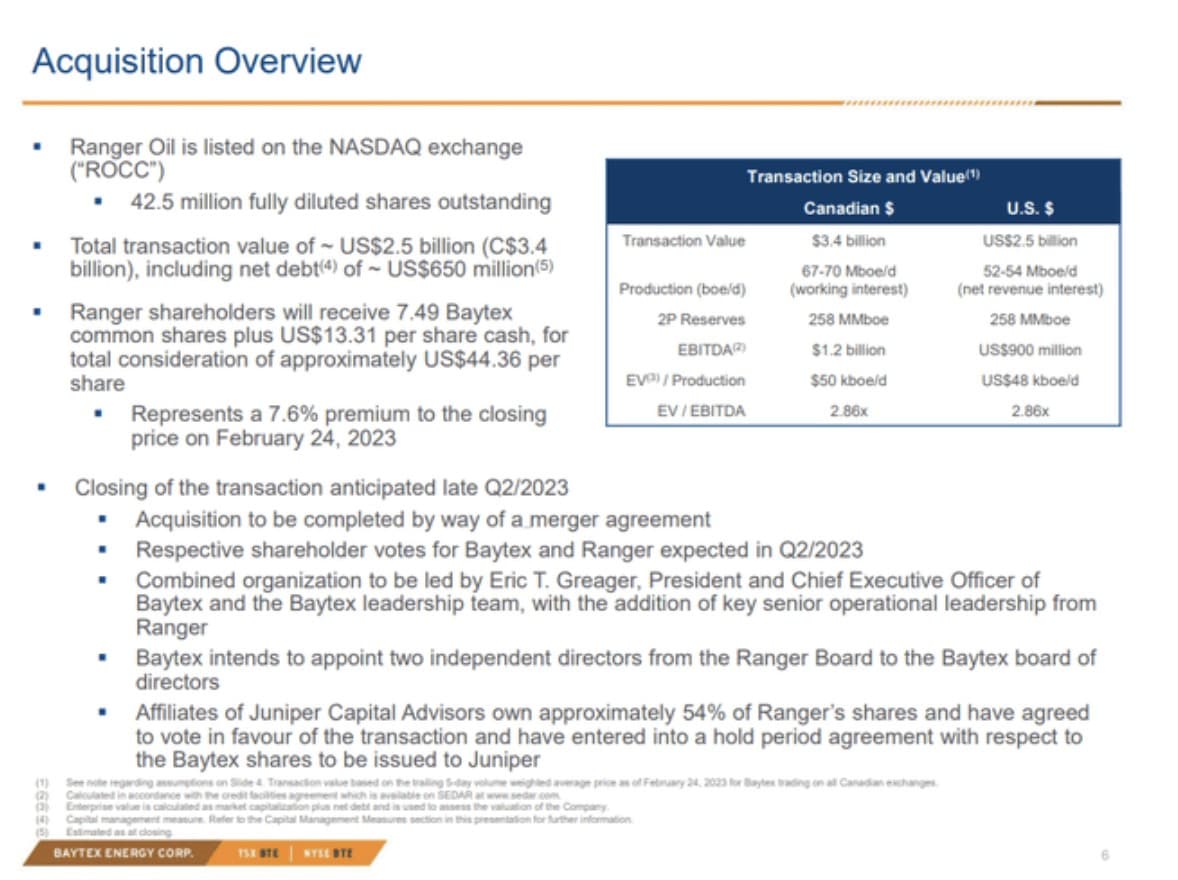

When all the “T’s” are crossed and the “i’s” dotted on this deal, BTE will have vastly increased its scale in this vital basin with ready access to the Corpus export market. More importantly, it brings production without the “tax” of the Western Canada Select-WCS discount, currently in the mid-$20s per barrel. The acreage covered in the deal is yielding 87% light oil and nearly 800 new drilling locations. New locations are the lifeblood of an oil company, and BTE estimates these will enable 12-15 years of development without further acquisitions.

The terms of the deal don’t appear particularly onerous. The deal price of $44.36 USD is a modest 7.6% premium to the Feb 24th closing price. Consisting of mostly stock and debt assumptions results in a very attractive EV/EBITDA multiple of 2.88X. Baytex leadership will remain in place.

Here’s the key

The Ranger acreage lies almost entirely in the Tier I black oil strata of the Eagle Ford in Gonzales and Lavaca counties. This is noteworthy as it follows the strategy employed by Devon and Marathon in their recent Eagle Ford acreage pickups. I see the non-op stuff (MRO is operator) as an advantage, as it will give them access to MRO’s development strategy. Marathon Oil is a world-class operator able to compete with anyone in the market. In effect, although BTE is coming to a new area, they don’t have to reinvent the wheel with drilling or completion strategies. Long-time partner Marathon Oil has been making very successful wells in the Eagle Ford.

Along with the asset itself comes the experienced Ranger personnel now operating the fields. These folks have obviously been doing a great job managing the asset and nothing may change. Still it would be hard to think they wouldn’t tap the MRO database to which they now have access. Marathon has been making great wells in the Eagle Ford with some from the Ensign pickup making IP: 30’s of 2,500 BOPD. If BTE can match performance like that from their acreage (in the same Gonzales/Lavaca counties as MRO), this will turn out to be a very good deal indeed.

Cash Flow improves 2023-2026

BTE cash flow as a standalone was on a positive track that is enhanced by about 23% with the assets of the merged company. With breakeven in the low $40’s and without the WCS discount, the Eagle Ford assets put new money in BTE’s pocket from day one. It also works to smooth out cash flow troughs, like the one the WCS discount is currently imposing, with light oil production ready to access a wide open export market.

Risks to the thesis

There is always the risk the deal may not close. There are no rumblings about this that I could discover in preparation for this article. The fact remains that both Baytex and Ranger are off their share prices as of the 24th of February, 2023, by about 15%. The turn in oil prices is taking the shares of both back toward this level, but the risk must be noted.

The combined company’s debt will be ~ $2.4 bn USD, or one turn of EBITDA. That’s a lot of carrying cost and needs to be reduced ASAP. The company notes this as a focus, but its ability to pare it down depends on its $75 oil price assumption. We think this risk is modest as oil prices are predicted to rebound during the year. Goldman Sachs, (NYSE: GS) has recently put out a forecast for a quick rebound to $90 in Q-2, and a YE 2023 exit price of $107 for Brent. Modest or not, the debt presents a worst-case risk to the thesis.

Your takeaway

BTE/Ranger presents a pretty compelling picture as a combined company. As noted above, the combination will trade under 3X EV/EBITDA, and about 3.5X forward cash flow. BTE is trading at $34K per barrel on a forward price per flowing barrel basis. Those are fire sale multiples for a company with the combined assets of the two. BTE expects the deal to be consummated with Ranger in Q-2, of 2023.

Analysts rank the company as Overweight , with a modest CAD upside to $7.40 from the current $5.40. That clearly predates the Ranger announcement, and I expect updates will boost the marketability of the stock, which has also been recently enhanced with an NYSE listing with the same symbol as their TSX listing-BTE.

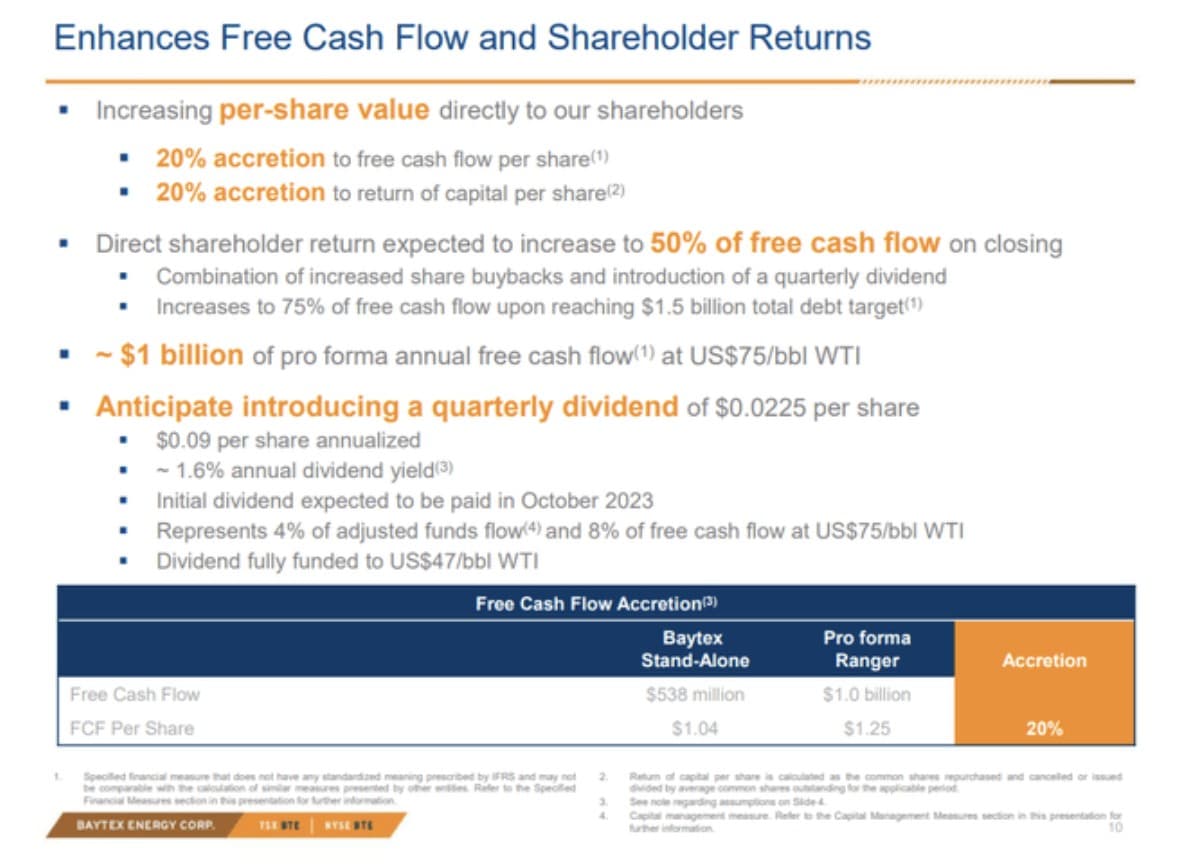

As the slide below indicates, BTE/Ranger is not just a growth proposition. The Ranger deal looks clearly accretive to me, and BTE is forecasting ~$1.2 bn USD in free cash this year at $75 WTI. That opens the door to shareholder returns to which the company discusses in their deal packet, with 50% of Free Cash on closing, advancing to 75% on meeting debt reduction targets.

As you would expect, most of this commentary has been about the Ranger deal. No article on BTE is complete without a quick note on their progress with their core acreage in the Peavine, Clearwater plays. BTE is making solid progress with this low-cost, low-decline asset as noted in the IP: 30’s below. Natural Gas Intel, calls this the “most economic play in North America.’

Bottom line, I think BTE makes an attractive case for new investment or addition to standing positions at current prices. We’ve established that the current downdraft impacting oil prices is ending soon, thanks to well-noted upticks in Chinese demand and a stabilization of the banking sector. It’s early in this reappraisal of oil prices, meaning that folks who pick up shares of BTE now should be rewarded with near-term gains as the rebound continues.

Source: https://oilprice.com/